If You Are A Plan Sponsor, You Are a Plan Fiduciary

A retirement plan sponsor has obligations and responsibilities to its employees who participate in the retirement plan.

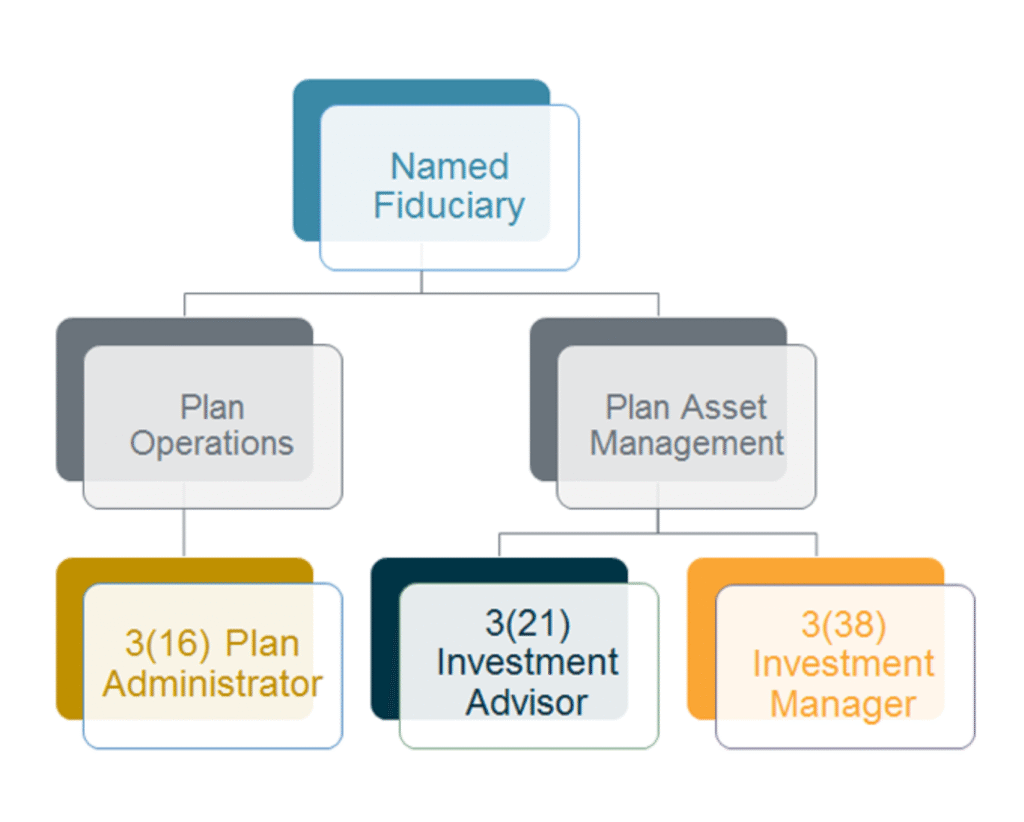

Through the Named Fiduciary, the sponsor has the duty to make prudent decisions with regard to the plan and to make such decisions solely in the interest of the plan’s participants. This person or group is named in the plan and is authorized to oversee the plan’s operation and administration and is responsible for plan asset management. The Named Fiduciary can be considered the Fiduciary-in-Chief.

The Plan Administrator: Your COO

The Plan Administrator is also named in the plan and is directly responsible for plan administration. The Plan Administrator can be considered the plan’s Chief Operating Officer.

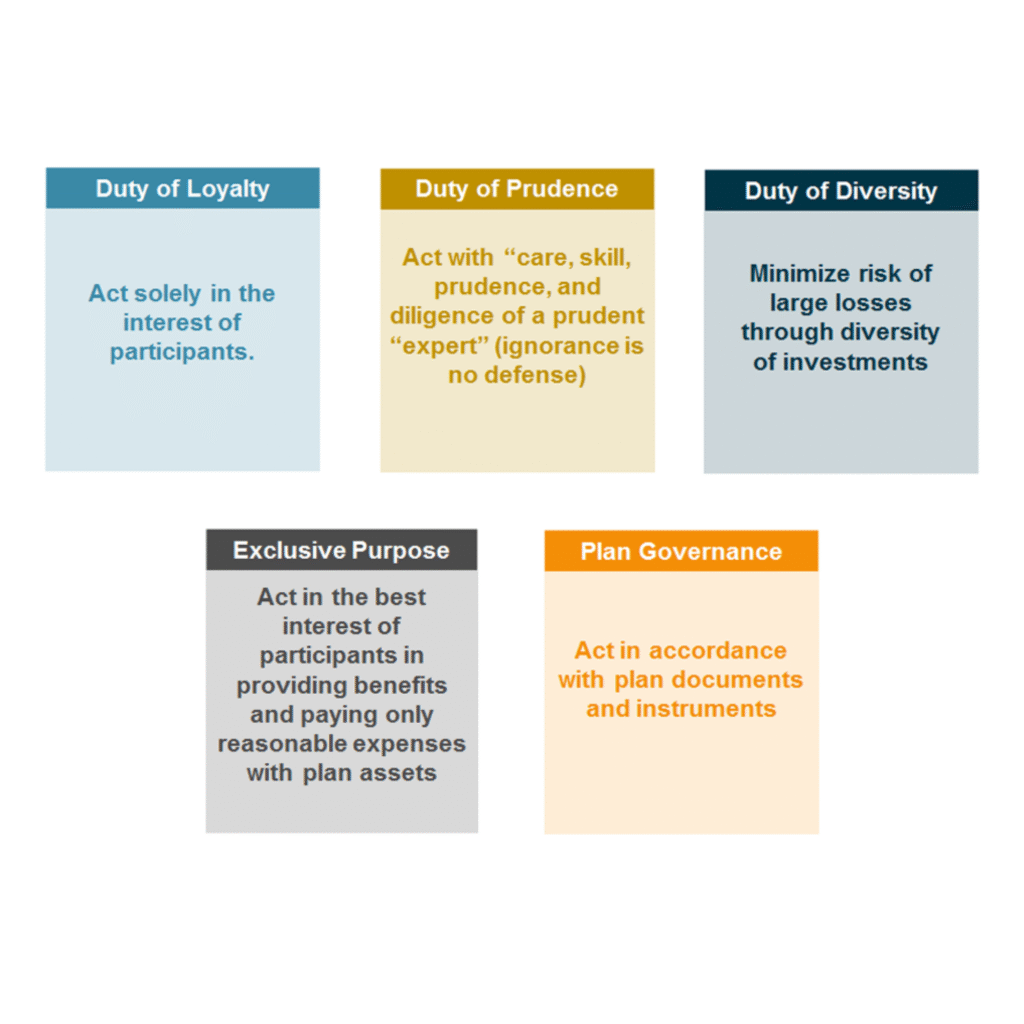

Under ERISA, a plan fiduciary must meet these core fiduciary standards:

Where does a Fiduciary get assistance?

Plan Administration: The Plan Administrator will typically hire a record keeper and a Third Party Administrator (TPA) to assist in plan administration. These entities are not typically fiduciaries; they perform ministerial services at the direction of the Plan Administrator.

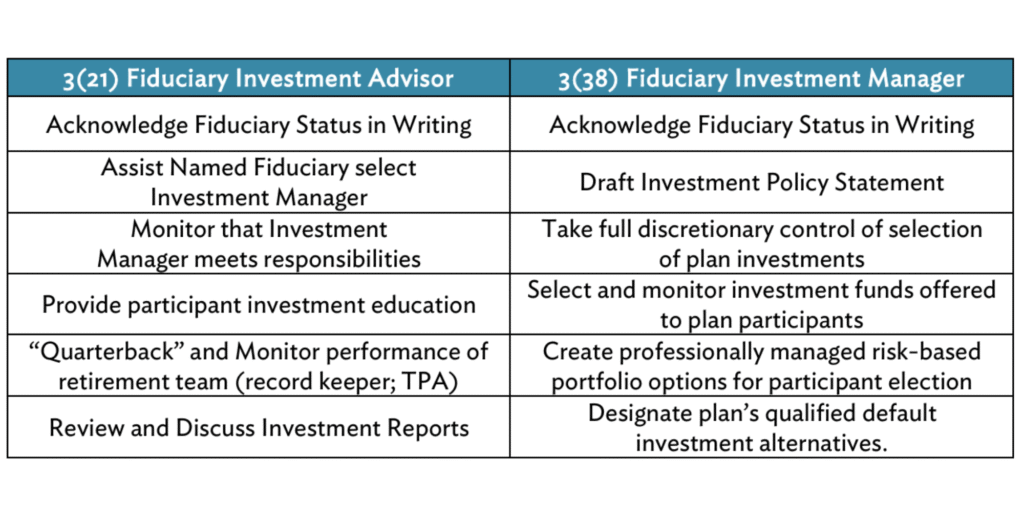

Plan Asset Management: The Named Fiduciary may hire investment advisors to meet its duty of prudence with respect to asset management. By using a combination of a 3(21) Fiduciary Investment Advisor and a 3(38) Investment Manager, the Named Fiduciary can avail itself of partners that specifically accept fiduciary status under the plan. Fiduciary partners will, and must, act in the best interest of participants in the performance of their duties.

The 3(21) Investment Advisor shares fiduciary duties with the Named Fiduciary while the 3(38) Investment Manager will accept full fiduciary responsibility for selecting and monitoring the investment options offered under the plan.

What if a Fiduciary breaches its duty?

Fiduciaries are liable for their fiduciary decisions. To limit personal liability, fiduciaries must understand their duties to the plan and plan participants. ERISA strictly prohibits fiduciaries from dealing with plan assets in own interest, in engaging in transactions involving the plan on behalf of a party whose interest is adverse to the interests of the plan or plan participants, or receiving consideration for their own accounts from a party dealing with a plan asset transaction. As a general rule, transactions between a plan and its fiduciaries are prohibited unless the transaction is exempted under ERISA or the Department of Labor has issued a prohibited transaction exemption under ERISA.

The best way to avoid fiduciary problems is to do what is right for participants. Acting in participants’ best interests is your best fiduciary defense.

Take the Guesswork Out of Fiduciary Responsibility

Managing a retirement plan shouldn’t feel like walking a legal tightrope. At PlanSimple, we help business owners build smart, compliant retirement plans backed by the right team of fiduciary and administrative support.

Whether you’re evaluating your current setup or starting fresh, we’ll guide you through the process so you can protect your people—and your peace of mind.

Let’s connect to review your plan, reduce your risk, and simplify your responsibilities.

👉 Click here to schedule a no-pressure consultation today. Your future (and your employees’) will thank you.

This information was developed as a general guide to educate plan sponsors and is not intended as authoritative guidance or tax/legal advice. Each plan has unique requirements, and you should consult your attorney or tax advisor for guidance on your specific situation.

PlanSimple Financial Partners, LLC is a registered investment adviser located in New Orleans, Louisiana. PlanSimple Financial Partners, LLC may only transact business in those states in which it is registered, or qualifies for an exemption or exclusion from registration requirements. Investment Advisory Services are offered through PlanSimple Financial Partners, LLC, a registered investment adviser.