401k Consulting Division

We help drive retirement readiness by providing employees with comprehensive plan support, resources, and tools.

Unlock the Full Potential of Your 401k Plan with PlanSimple

As an employer offering a 401k plan, you understand the importance of providing a secure financial future for your employees. However, navigating the complexities of fiduciary responsibilities, complying with regulations, plan performance, fees, and participant engagement can be overwhelming. That’s where PlanSimple comes in.

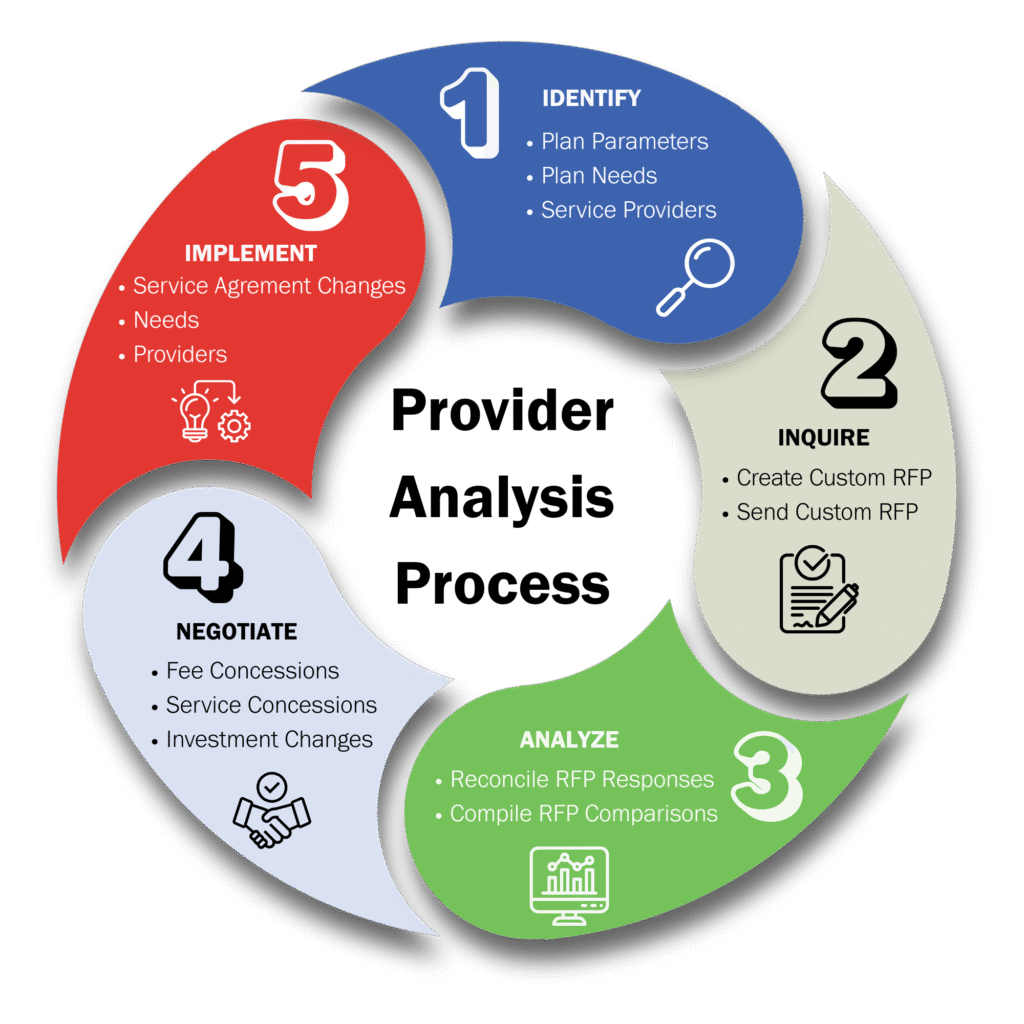

Selecting and monitoring service providers is one of the most important duties that retirement plan sponsors and fiduciaries must do. Our proprietary benchmarking process incorporates a plan’s parameters, complexity, investment lineup, service requirements and other unique considerations in order to determine a reasonable fee for a plan’s recordkeeping and administrative services.

Here’s how this works:

- Our live-bid, RFP process ensures apple-to-apple comparisons are used throughout the evaluation process.

- All fee comparisons are based on current market prices rather than a database of historical recordkeeping fees.

- Over 400 recordkeeping data points are compared side-by-side to balance cost and quality considerations.

- Competitive bidding with multiple providers maximizes a plan’s negotiating leverage.

"It's the Right Time for the Right Partner."

Managing fiduciary obligations is a crucial aspect of running your business, and we understand that every employer has unique preferences. Whether you prefer to manage fiduciary responsibilities yourself, seek some assistance, or have someone manage them on your behalf, PlanSimple is here to help. We ensure that your company remains audit-ready, allowing you to focus on the core aspects of your business.

How Can PlanSimple Help Me?

Integrated Approach to Retirement Readiness

We offer a variety of tools and solutions to educate your employees and give them the right information to drive retirement readiness. Our solutions are both simple and comprehensive; this helps your employees know where they stand and where they’re going.

Plan Expertise

We’ll simplify the plan setup and conversion process with minimal disruption for your employees and staff. And our ongoing support system will help make managing your plan easier. Additionally, we provide thought leadership and serve as your partner by breaking down challenges and offering clear solutions.

Participant Driven Culture

Our financial wellness program is paramount to the success of your Employer Sponsored Retirement Plan. We are committed to your employees and offer support every step of the way.

FAQs

What are the benefits of offering a 401(k) plan to employees?

The main benefits of offering a 401(k) plan to employees are the ability for employees to save and defer income into their retirement accounts, as well as the potential tax savings and employer contributions. The tax advantages can provide additional incentive for employers to offer 401(k) plans, since they may be able to deduct some or all of the employer contributions. Additionally, offering a 401(k) plan can help employers attract and retain top talent by offering a competitive benefits package.

How much does it cost to set up and administer a 401(k) plan?

The cost of setting up and administering a 401(k) plan can vary significantly, depending on the complexity of the plan and the provider you choose. Generally speaking, setup costs can range from $500 to $2,000 or more. Ongoing administrative fees typically range from 0.5% to 3% of assets in the plan each year, depending on the size of the plan and number of participants. It’s important to shop around and compare costs when selecting a 401(k) provider. Additionally, some providers offer discounts for larger plans with more participants.

How often should I review and update the 401(k) plan to ensure it remains competitive and meets the changing needs of my employees?

It is important to regularly review and update your 401(k) plan every year to ensure it meets the changing needs of your employees. Specifically, you should review any changes in tax laws or other regulations that apply to the 401(k) plan, compare the benefits offered with those provided by other organizations, and consider new features such as higher contribution limits or expanded investment options. A full scope RFP should be executed every 3-5 years to ensure your plan is properly benchmarked and, as a plan sponsor or administrator, remain compliant with your fiduciary responsibilities.

Are there any tax advantages for employers who offer a 401(k) plan?

Yes, employers offering a 401(k) plan can receive several tax advantages. These include reduced income taxes on employer contributions, deferred taxation of employee contributions, and potential deductions for startup costs. Additionally, employers may be able to deduct administrative and maintenance expenses related to the 401(k) plan. Employers also have the option of establishing a matching contribution program and deducting those contributions made to employees’ accounts. Finally, employers may receive credits or other incentives from their state governments if they offer retirement plans which include employer-provided educational materials about retirement planning as part of their 401(k) plan design.

How can I ensure my employees understand the importance of saving for retirement and make the most of their 401(k) accounts?

The best way to ensure your employees understand the importance of saving for retirement and are making the most of their 401(k) accounts is to align the plan with an advisor and plan provider that focuses on financial wellness. This type of program can include offering workshops on saving for retirement, online tools and resources, or having an annual review session with each employee to go over retirement savings goals. Additionally, employers can help bridge the gap between the resources available and its participants by allowing the employee to engage the plan advisor while on-site. Offering these resources will help ensure that your team understands the value of saving for retirement and makes the most out of their 401(k) accounts.

Can I offer additional retirement savings options alongside a 401(k) plan, such as a Roth IRA or profit-sharing plan?

Yes, employers may offer additional retirement savings options in addition to a 401(k) plan. Other types of retirement savings accounts include Roth IRAs and profit-sharing plans. It is important to evaluate the different types of accounts and determine which ones best meet the needs of your employees before offering them as an option. Additionally, you may want to consult an attorney or tax professional for specific guidance on setting up these plans.

FAQ (ESTABLISHED PLANS)

As a plan sponsor, what should be my main concern with our 401k plan?

While there are a variety of concerns when it comes to sponsoring a retirement plan, the overarching fear for most of our clients that we onboard is that they aren’t adhering to their fiduciary responsibilities. This is a broad term for many different obligations, but the typical area of improvement is benchmarking the plan fund lineup, which keeps the funds competitive with their peer group.

How often should I consider alternative providers?

We highly recommend that you undergo a complete RFP analysis every 3-5 years to ensure that your plan is priced competitively, as well as making sure you are receiving benefits from your provider that are comparable to your peer’s benefits. As an example, we see it all too often where Company A was not offered the same Education and Financial Wellness program as Company B, simply because nobody thought to ask or negotiate on Company A’s behalf. Our benchmarking and RFP process will help determine what areas of improvement exist and gives us concrete data that helps us negotiate services.

We work directly with the Provider. How can you and your team help?

The PlanSimple Retirement Plan Division can work on a project basis and help assess the current plan fees and services. Each plan is different, but we are confident that a simple conversation can result in a significant impact on your plan participants.

What is the difference between Institutional-Level Due Diligence and Standard Due Diligence?

Our process incorporates a proprietary, quantitative fund Scorecard (insert TM) and a thorough qualitative review of your fund lineup, plan fees and expenses, and financial wellness programs. We have separate scoring methods for active versus passive fund managers, custom benchmark indexes and risk-based peer group reviews that ensure accurate comparisons.

What are some tips to keep me in compliance with the DOL?

- Establish a process for comparing and selecting funds, including Target-Date Funds (TDF’s)

- Establish a process for regularly reviewing your fund lineup

- Regularly review and compare your fund’s fees and investment expenses

- Develop and implement effective employee communication

- Document the above processes and warehouse notes from each committee meeting

- When in doubt, contact us and we can help answer any questions with our team of ERISA Attorneys available

Take the next step toward optimizing your 401(k) plan with PlanSimple.

Contact us today to schedule a consultation and unlock the full potential of your employees' retirement savings.