Record high inflation and negative economic growth, as measured by US GDP growth, have fueled recession fears. The bond market is similarly flashing recessionary signals. Despite this, the S&P 500 through Friday, August 5, 2022, has rallied 13% higher than its June 16 bear market low[1], making the current environment a head-scratcher for many.

Economic Data Flashes Mixed Recession Signals

The July 2022 jobs report showed an addition of 528,000 jobs, and worker pay grew by 5.2% year-over-year, both higher than expected.[2] The unemployment rate ticked down to 3.5%, tied with the lowest on record since 1969.[3] The US economy has now regained the 22 million jobs lost during the pandemic.[4] This data took many by surprise, as it followed another record high inflation reading of 9.1% in June and two consecutive quarters of negative economic growth for the US, a common definition of a recession but not the official definition.[5]

Source: FRED. Data as of July-2022

There is no historical precedent to indicate an economy in a recession can produce continued job growth and support a historically low unemployment rate. As such, the debate of whether we are in a recession will continue until we hear from the officials at the National Bureau of Economic Research, who often take months to make the official call after the fact.

For investors, the debate is less important than what lies ahead. Based on the latest record job and wage growth, the Federal Reserve will likely continue on its path to raising interest rates at a similar pace to the last few months, increasing the potential for a policy error-led recession.

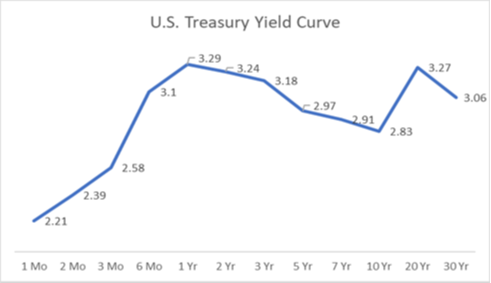

Bonds are Flashing a Recessionary Signal

Another closely watched predictor of a potential recession is the bond market. Known as the inverted yield curve, it has flashed a recessionary warning signal. The yield curve shows the relationship between interest rates across different maturities for a set of similar bonds. The most commonly referenced yield curve is the US Treasury. The Treasury rates drive the interest rates on things like your mortgage or the rate you earn on CD, which makes this yield curve a closely watched benchmark for the state of the economy.

Typically, the curve is upward sloping, which means investors who purchase bonds with shorter maturities expect a lower yield, but those who purchase longer bonds expect to get paid extra for taking a longer risk of inflation and other uncertainties. On the other hand, an inverted yield curve is when short-term interest rates are above rates for long-term government debt. The fear is that this stops companies from investing as short-term borrowing becomes expensive, which may, in turn, cause a recession.

Source: FactSet. Data as of 5-Aug-22

Today, while the overall shape of the yield curve remains upward sloping, many key parts remain inverted. According to Ned Davis Research, when 55% of the yield curve has inverted, the probability of a recession in the coming months greatly increases.[6] As of August 5, 53% remains inverted providing a flashing recessionary signal.

Stock Market Rally a Head Fake?

Despite the recession debate, the S&P 500 has gained 13% from the bear market lows of June 16 and is now down 12.2% on the year and 5.0% over the past year.[7] This may be a surprise considering what investors have lived through.

The stock market and the economy, while linked, are not one and the same. Stock markets look ahead, while the economy is a look in the rearview and tends to lag. Those that believe the economy is not in a recession may attribute the rally in the stock market to the strong job market despite record high inflation, or that corporate earnings have been better than expected.[8] For those who believe a recession is yet to arrive, the latest rally is simply a bear market rally from investors jumping in for fear of missing out, and similar to other bear markets may plunge again before fully recovering.

While we won’t know the longevity of the latest rally, we do know that not all bear markets are created equal. Since WWII, there have been twelve bear markets. Eight out of 12 coincided with a recession and saw a median decline of 35%, while those not associated with a recession have seen a median decline of 28%.[9] In 2022, the worst decline from peak to trough was roughly 24% in the S&P 500.[10] It is likely the bear market will not be over until the recession arrives or the risk of a recession has been stamped out.

Source: Goldman Sachs Investment Research and Goldman Sachs Asset Management. Data as of May 2022

Conclusion

The debate over whether or not we are in a recession and whether the latest rally is sustainable will surely continue. Recessions and the markets are always hard to predict but the current environment is confusing. There are so many opinions and conflicting data sets that it’s difficult to have clarity today, let alone predict the future.

Perhaps the one thing investors can take solace in knowing is that economic and market expansions last far longer than recessions and bear markets. Investors have generally been rewarded for their time in the market versus timing the market.

[1] FactSet

[2] Bureau of Labor Statistics. Data from July 2022

[3] FRED. Unemployment Rate Since 1969

[4] https://www.usatoday.com/story/money/2022/08/05/july-jobs-report-unemployment-rate-3-5-528-000-jobs-added/10243309002/

[5] Bureau of Labor Statistics. June Inflation REport

[6] Ned Davis Research. Stagflation? July 19,2022

[7] FactSet. Data as of 8/5/2022

[8] https://www.reuters.com/markets/us/us-corporate-profits-economic-outlooks-surprisingly-upbeat-2022-08-02/

[9] https://www.gsam.com/content/gsam/us/en/institutions/market-insights/gsam-connect/2022/market-minute-context-on-bear-markets.html

[10] FactSet

IMPORTANT INFORMATION

This is for informational purposes only, is not a solicitation, and should not be considered investment, legal or tax advice. The information in this report has been drawn from sources believed to be reliable, but its accuracy is not guaranteed, and is subject to change. Investors seeking more information should contact their financial advisor. Financial advisors may seek more information by contacting AssetMark at 800-664-5345.

Investing involves risk, including the possible loss of principal. Past performance does not guarantee future results. Asset allocation cannot eliminate the risk of fluctuating prices and uncertain returns. There is no guarantee that a diversified portfolio will outperform a non-diversified portfolio. No investment strategy, such as asset allocation, can guarantee a profit or protect against loss. Actual client results will vary based on investment selection, timing, market conditions, and tax situation. It is not possible to invest directly in an index. Indexes are unmanaged, do not incur management fees, costs and expenses and cannot be invested in directly. Index performance assumes the reinvestment of dividends.

Investments in equities, bonds, options, and other securities, whether held individually or through mutual funds and exchange traded funds, can decline significantly in response to adverse market conditions, company-specific events, changes in exchange rates, and domestic, international, economic, and political developments.

AssetMark, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission. AssetMark and third-party service providers are separate and unaffiliated companies. Each party is responsible for their own content and services.

©2022 AssetMark, Inc. All rights reserved.